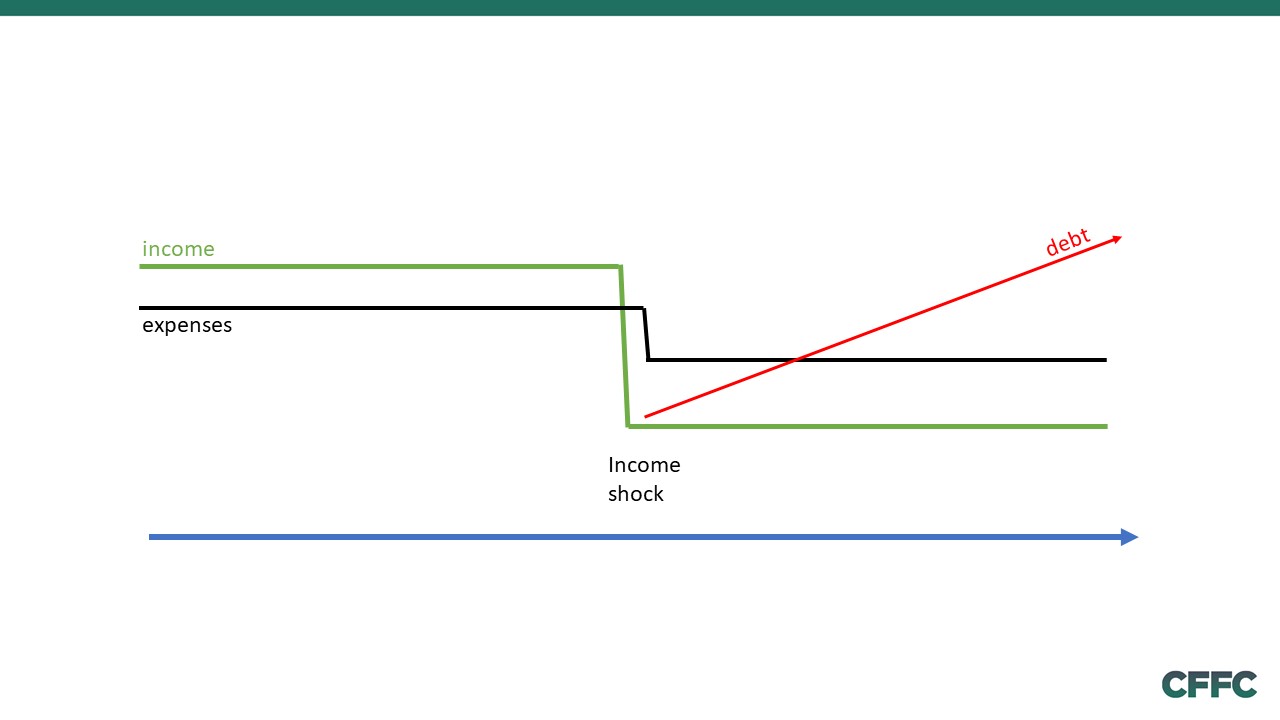

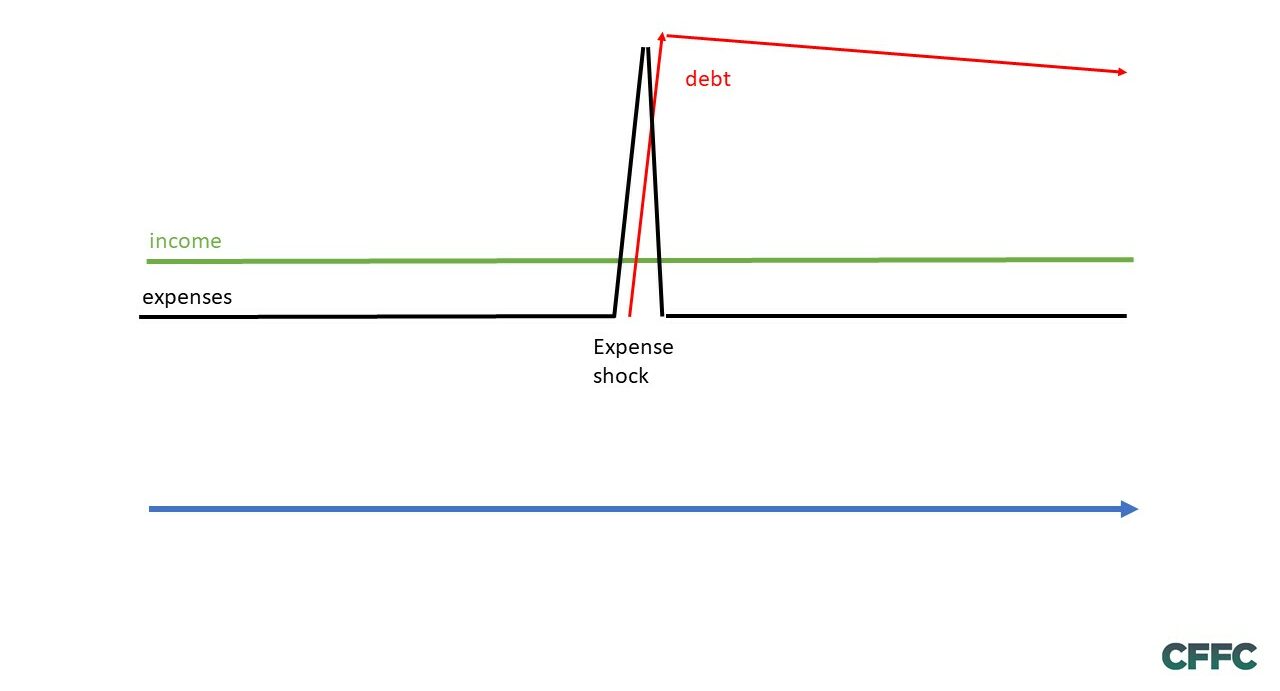

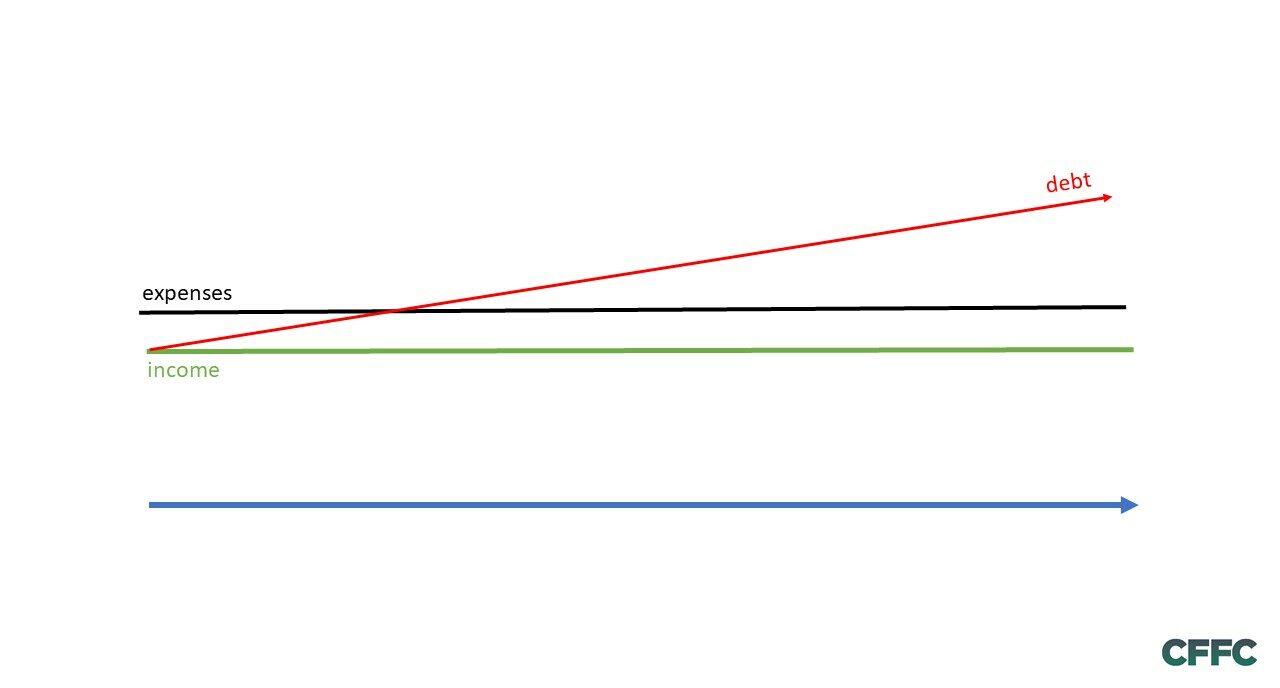

Three reasons why people end up in debt

August 10, 2021

Blog

What is sexually transmitted debt (STD)?

Like other forms of STDs, sexually transmitted debt is something you can catch from your partner. Sexually transmitted debt, or STD, is often used to

Read More »

Real life story

How Toni took back control of her debt

Toni, a sole parent with three children, one of whom requires full time support, was living week to week. Toni works from home as an

Read More »

DEBTsolve

Our DEBTsolve programme will help you take control of your unmanageable debt. Our specialist Financial Wellbeing Coach will work with you to understand your situation

Read More »