Abbie plans for a debt-free life after economic harm

Facing my finances and past head-on wasn’t easy — but with practical and empathetic support, it freed up my life again.

Today I’m lighter, more confident and planning for the future. I’m proud to be rebuilding a secure and happy life for me and my son.

This is Abbie’s story, edited to keep her from being identified and to help you read. Quotes are Abbie’s own words. Names have been changed.

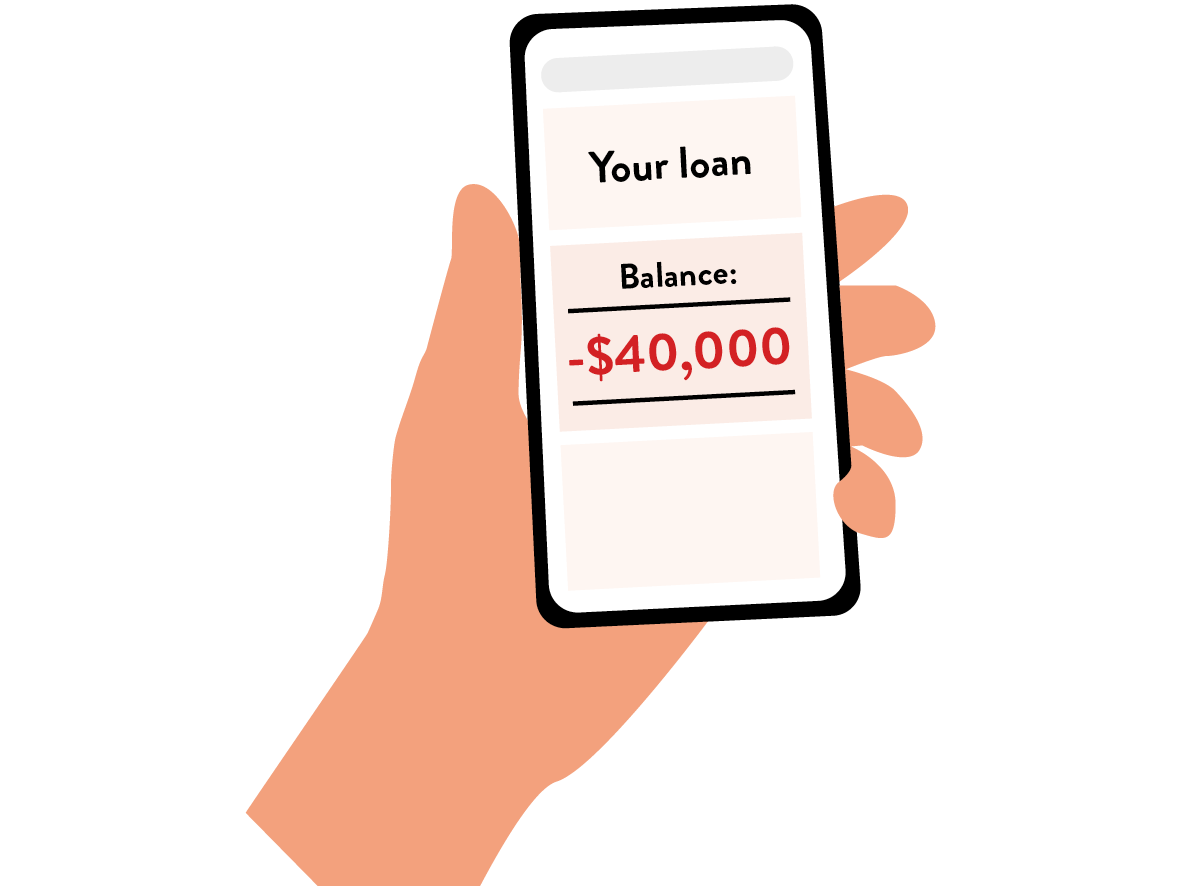

I had just come out of a string of abusive relationships, one of which left me in significant financial trouble by taking out loans in my name that he never repaid. When my car broke down, I was buried in debt with no credit and no real support to help me through.

Reaching out to Good Shepherd was one of the best financial decisions I ever made. When I first got in contact, I was hoping to get a loan for a car — but I ended up getting so much more.

Once Good Shepherd’s loan team heard more about my experience, they put me in touch with Charlotte in their economic harm team. Her support was beyond anything I could have imagined. Charlotte reached out to all my creditors and negotiated with them, managing to erase nearly $12,000 worth of debt.

The process did bring some challenges. It was long-winded, with a lot of paperwork and financial details to sort through. At times, I wasn’t sure if I’d be approved for the loan because of all the debt I was carrying. The process also forced me to face my finances — and the aftermath of those abusive relationships — head-on and confront things I had been avoiding.

“I had been hiding from it with my head in the sand, which is what you do when you are completely overwhelmed. It was a very hard time — but when the loan came through, the relief that I felt. Everything was worth all the work.”

I’ve always found it hard to ask for help, especially after everything I’d been through. But Charlotte was incredibly understanding. She had been through a similar experience, which made things easier. She was always there for me, checking in with updates as she worked hard behind the scenes to clear all those debts. It’s hard to explain how important it felt to have someone who genuinely cared about my situation. Charlotte didn’t judge me but instead helped me turn things around.

“Who was this amazing person who came into my life at the right time?…I felt completely blessed.”

There were some immediate changes in my life after working with Charlotte and Good Shepherd. It was such a relief to clear most of those debts and to have a good working car again. It was also an important starting point for a life that felt like my own again.

“I said to [Charlotte] that she came into my life and helped me remove those awful exes in my life bit by bit. I feel freer. I feel more ordered. And that’s a good and secure place to be in.”

I haven’t missed a payment with Good Shepherd yet, and I’ve been able to increase my payments too. My finances are much more in order. I no longer feel burdened by the debts that once seemed impossible. I know exactly what I owe and what’s coming out each month. I finally have the ability and confidence to save and make decisions I couldn’t have made before.

My son has a birthday coming up. I’m able to afford a little birthday party. That’s a huge shift for us, both financially and emotionally. It feels so good to be able to contribute to school fundraisers and events — things that may seem small to some, but make a huge difference to me.

“[My son] had photographs taken…that were beautiful. I was able to buy four of them. These sorts of things make an impact on you and him and your parenting, and make your child feel valid too.”

I even just bought a self-propelled lawn mower, something I have managed to save up for. It wasn’t a huge expense but the ability to make that purchase was something that felt out of reach before.

I’m feeling so much more stable these days. Money is still tight, but I have enough to live — and I get to enjoy precious time with my son while he’s still young. I don’t spend on things I don’t need. I’m proud of that. But I can afford to take myself out to dinner every now and then without too much stress. I can just enjoy the moment.

Looking ahead, I hope to be completely debt-free in five years. I want to have a steady income and a routine that supports my family. I’m also thinking about going back to study, possibly in healthcare, which feels like the right path for me based on my own experiences with injuries. I want to help others the way I’ve been helped. In the meantime, I am thankful for where I am now. Good Shepherd’s support has made such a big difference in my life.

“I’m very grateful…It was just at such a turning point in my life. No actually, this whole thing was the turning point at a really tough time.”